Deducting motor vehicle expenses: Gardner v The Queen

A recent Tax Court decision provides guidance for taxpayers working from home during the COVID-19 pandemic

Introduction: Gardner v. The Queen (2020)

|

COVID-19 has upended traditional work structures and resulted in many taxpayers working from home, writes David J. Rotfleisch, CPA, CA, JD, of Rotfleisch & Samulovitch P.C. |

The appellant, Ms. Gardner, was reassessed by the Canada Revenue Agency in 2016 and denied motor vehicle expenses claimed for the 2015 taxation year. When Ms. Gardner filed her 2015 income tax returns, she claimed motor vehicle expenses under paragraph 8(1)(h.1) of the Income Tax Act (the "Tax Act") amounting to $12,868. During the 2015 taxation year, she was employed by Coty Canada Inc. (the "Employer"), which has an office located in Oakville.

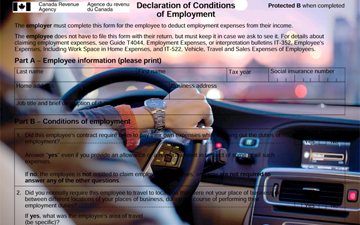

However, Ms. Gardner primarily worked out of her home office located in Pickering, and only travelled to the Employer's office infrequently. In support of her claimed motor vehicle expenses, the Employer completed a Form T2200 "Declaration of Conditions of Employment" pursuant to subsection 8(10) of the Tax Act. In the prescribed form, the Employer stated that her employment contract required her to perform 90% of her employment duties from her home office, and that she did not have access to a company vehicle. Ms. Gardner used her personal vehicle to travel to the Employer's office, located 72 kilometres from her home, for meetings with supervisors and co-workers once or twice a week. Furthermore, she neither had her own office at the Employer's office, nor did she work there on a regular basis.

Appeal to the Tax Court of Canada to allow motor vehicle expenses

Ms. Gardner appealed to the Tax Court of Canada [Gardner v. The Queen, 2020-10-02] to allow the claimed motor vehicle expenses. Her position was that she was required to carry on her employment duties at her home office, and that any travel between her home office and the Employer's office was travel between two places of employment. Conversely, the Crown argued that Ms. Gardner was traveling from her home, not her home office, to the Employer's office, therefore she was unable to deduct motor vehicle expenses for the 2015 taxation year. Neither party disagreed with respect to the amount claimed as motor vehicle expenses.

Did the travel between locations constitute employment travel or personal travel?

The core issue in this appeal was whether the travel between Ms. Gardner's home and the Employer's office was personal travel or employment travel. Under subparagraph 8(1)(h.1)(ii) of the Tax Act, motor vehicle expenses can only be claimed when incurred for travelling in the course of employment. If the travel was personal travel, motor vehicle expenses would not be allowed, whereas if it was employment travel, the expenses would be allowed. If allowed, Ms. Gardner would be able to deduct the motor vehicle expenses from her income for the 2015 taxation year.

The Tax Court held that Ms. Gardner was travelling between her home office and the Employer's office in the course of her employment and allowed the claimed motor vehicle expenses. The basis for this decision was that Ms. Gardner travelled between two employment-related locations.

What constitutes travel between two employment-related locations?

The Tax Court held that Ms. Gardner traveled between two employment-related locations, therefore she incurred motor vehicle expenses from employment travel. Ms. Gardner cited the Tax Court's informal decision in Campbell et al v R. ("Campbell"), 2003 TCC 160, for the proposition that travel from a home office, where much of the employment work is done, to an employer's place of business for meetings constitutes employment travel. In Campbell, the taxpayers were employed by a school board and primarily worked from their home offices but attended the school board's main office, where they did not have offices, for regularly scheduled meetings. In that case, the Tax Court held that the taxpayers were carrying out the duties of their employment when they travelled between locations.

Furthermore, the Tax Court did not consider it significant that after the taxpayers came home, they "might have gone to bed or turned on the TV or had a sandwich or raided the refrigerator." In Gardner, the Crown instead relied on McCreath v Her Majesty ("McCreath"), 2008 TCC 595, where the Tax Court rejected a taxpayer's claim for travel expenses on the basis that the taxpayer had an office available for him at the employer's place of business, but nevertheless chose to work at his home office, where he also did unrelated work.

The Tax Court distinguished Campbell and McCreath on the basis of the availability of office facilities at the employer's place of business. In Gardner, the evidence was clear that the Employer did not have an office available for Ms. Gardner, therefore she was required, as a condition of her employment, to work from her home office and travel between the two employment-related locations for meetings.

Claiming motor vehicle expenses as a result of COVID-19

The emergence of COVID-19 upended traditional work structures and has resulted in many taxpayers being required to work from home. Employees now required to travel between a home office and other employment-related locations may be eligible to deduct motor vehicle expenses for the 2020 taxation year.

However, before claiming motor vehicle expenses, taxpayers are required under subsection 8(10) of the Tax Act to obtain Form T2200, "Declaration of Conditions of Employment," which must be completed by their employer. The Canada Revenue Agency's interpretation bulletin IT-522, "Vehicle, Travel and Sales Expenses of Employees", states that taxpayers do not have to file Form T2200 with their return but must keep it in their records for examination on request.

David J Rotfleisch, CPA, CA, JD, is the founding tax lawyer of Rotfleisch & Samulovitch P.C., a Toronto-based boutique tax law firm. With over 30 years of experience as both a lawyer and chartered professional accountant, he has helped start-up businesses, resident and non-resident business owners and corporations with their tax planning, with will and estate planning, voluntary disclosures and tax dispute resolution including tax litigation. Visit www.Taxpage.com and email David at david@taxpage.com.

![]()

_20260711102711.png)

(0) Comments